Cargojet Inc. (TSX:CJT)(NYSE:CJT) had a stellar 2020. The pandemic sped up the company’s e-commerce delivery goals, and returns were never better. The company has since been expanding into even more areas for long-term growth.

Yet after earnings, shares in Cargojet stock plunged 10%. So what gives? Here we’ll look at why the stock dropped, and what investors should do next.

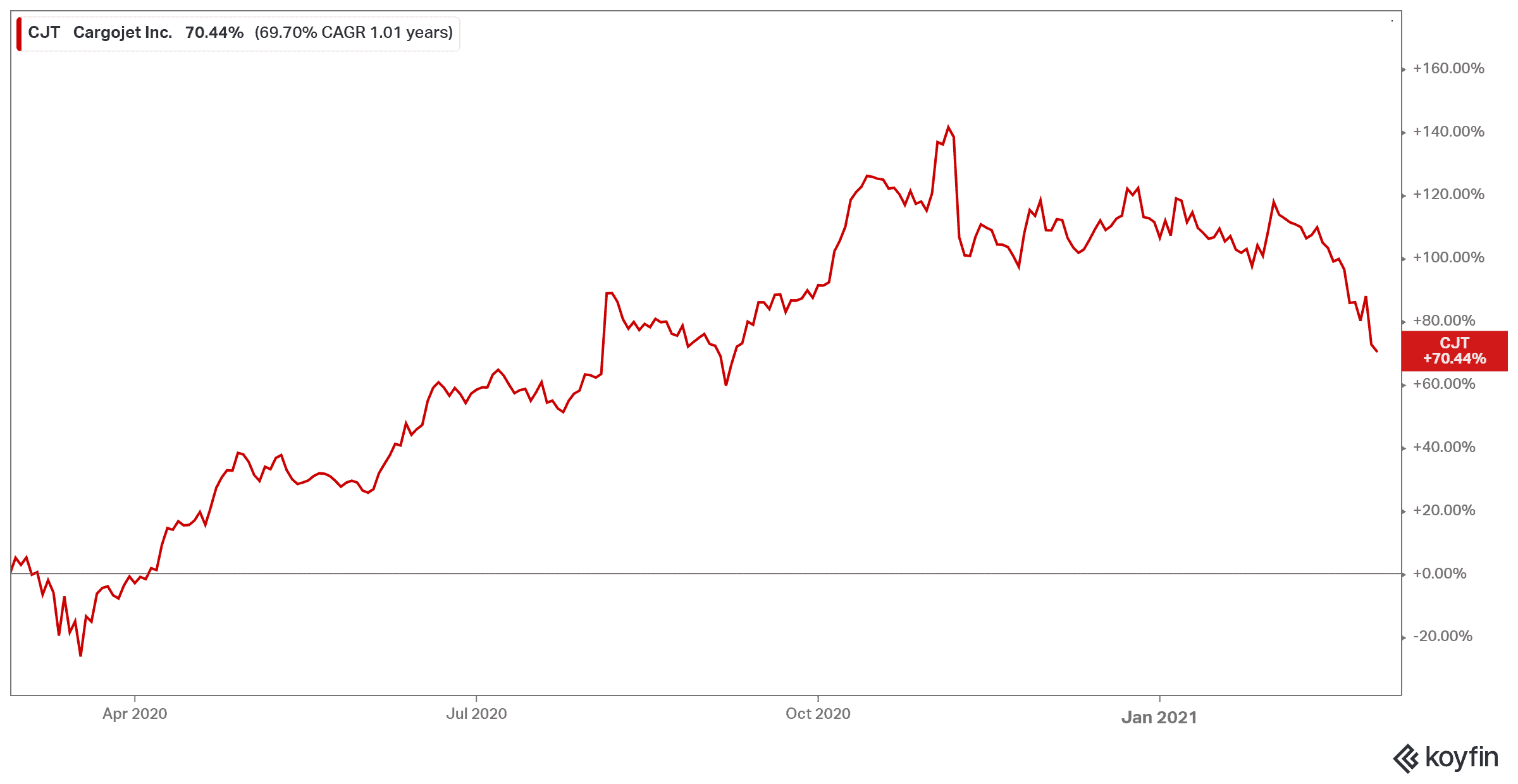

Why Cargojet sunk

Cargojet stock announced another strong earnings report for both the fourth quarter and full year. Total revenue was up 34% to $187.1 million for the fourth quarter, gross margin up 67%, and adjusted EBITDA 74%. So another stellar quarter overall.

The full year report was even more incredible, marking a transformation for the company. Total revenue was up 37%, gross margin up 110%, and adjusted EBITDA 87% compared to 2019. The balance sheet was incredible, with $196.8 million in free cash flow and $525 million in available liquidity. The company also announced it would be increasing its fleet to 28 all-cargo aircrafts after operating a record number of flights in 2020 and to further its international expansion.

So why the pullback? Investors believe the company may have peaked for a while. It’s not that analysts believe the stock is going to sink. Far from it. But look at the past year in the graph below, especially back to where shares hit a whopping $250.

As you can see, shares exploded in 2020 from the e-commerce boom. While other airlines relied on passengers, Cargojet stock exploded with the increase in cargo. And while it’s unlikely that we’ll see a return to pre-pandemic consumer habits, it may be that the stock has plateaued.

So what now?

I definitely don’t think you should give up on Cargojet stock. Far from it. If you own this stock, now is a great time to increase your stake or at least to hold. The company’s strong balance sheet alone tells you why this stock should be in your portfolio. Its healthy fundamentals mean it can afford to see a dip and continue to expand.

Management agrees. Chief Executive Officer Dr. Ajay Virmani stated during recent earnings that even with returning to pre-pandemic levels, the company is “embarking on the next phase of our growth by capturing international cargo opportunities. The disruption caused by vastly reduced passenger airline belly capacity has created new opportunities for international cargo that we are well positioned to go after.”

In short, this may only be the beginning of the company’s mega growth. Right now, it’s been mainly in North America. But the recent e-commerce boom and partnership with Amazon means Cargojet can now expand on an international level. Investors would do well to buy and hold this stock for decades as e-commerce continues to boom, providing more opportunities for this stock to soar.

Bottom line

If you’re an investor that sold shares in Cargojet after a bull run, I don’t blame you. But if you’re a long-term investor, don’t get scared after earnings. Earnings reports see dips and dives, but it’s the overall trends and fundamentals you should watch out for. In the case of Cargojet stock, its fundamentals are incredible.

Shares in the past five years are up 671% for a compound annual growth rate (CAGR) of 50%. Investors would do well to buy the dip and sit back and watch returns come in for decades.