Last week, energy stocks like Suncor Energy (TSX:SU)(NYSE:SU) drastically sold off on concerns around the COVID-19 Omicron variant. West Texas Intermediate oil (a good benchmark for North American oil prices) fell from US$78 on Thursday to US$68 on Friday — a 12% decline in one single day! This panic left some stock traders calling Black Friday Red Friday.

Despite being a large North American producer, Suncor was not immune to the sell-off. Its stock collapsed by almost 10% at one point on Friday. Since then, Suncor has been recovering some of its losses. However, it is still a large distance from its 52-week high set last week.

Image source: Getty Images

Is Suncor a stock to buy today?

Given this volatility, perhaps we should ask if this is an intriguing buying opportunity? I think it is, although there are some caveats. I will explain.

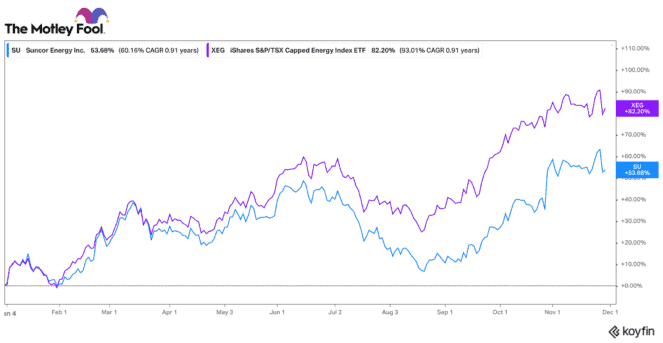

Suncor stock has had a great run in 2021. It is up 50% year to date! While that may appear impressive, its stock has actually lagged the broader S&P/TSX Capped Energy Index by almost 30 percentage points. Large oil and gas peers like Canadian Natural Resources and Tourmaline Oil have already surpassed their pre-pandemic price. On the other hand, Suncor still trades at a 25% discount to its pre-pandemic price.

There are a number of reasons for this. First, Suncor has had some significant operational challenges with a few of its projects. This has resulted in a few quarters that have slightly disappointed the market.

Second, unlike the two above stocks, Suncor actually slashed its dividend last year when oil prices collapsed. This may have permanently scared away a number of income-focused investors.

Finally, Suncor added on a bit more debt than some investors like. The above peers have pristine balance sheets that actually sustained and grew their dividends last year.

Suncor is doing a lot of things right

Despite some of these challenges, Suncor has also been doing a lot of things right lately. Since the pandemic, it has drastically reduced its cost structure. It has invested in technology to create operational efficiencies. Between US$35-$40 per barrel of oil, Suncor can actually cover its operating costs, sustaining capital, and its dividend. Any price above that becomes discretionary cash.

Right now, it is working on a five-year plan to further reduce overall costs and realize operational synergies. By 2025, its free cash flow breakeven, even after dividends, could actually be below US$30. This will help reinforce the sustainability and profitability of its business. Today, many of its past operational and maintenance issues are now resolved or complete. Consequently, this business is once again primed to hit its stride.

Suncor stock is yielding a ton of free cash

With oil at around US$70 per barrel, Suncor has been a cash flow machine. Last quarter, it produced $2.6 billion of funds from operations. With excess cash, it announced a 100% dividend increase, putting its dividend back to pre-COVID-19 levels.

Similarly,, it announced a plan to potentially buy back 107 million shares (or 7% of its float). Suncor continues to reduce its debt as well. Year-to-date, it has reduced its overall debt by $3.1 billion. Its debt is now below pre-pandemic levels.

Essentially, Suncor is operating better than it did before the pandemic. However, the market does not appreciate this. For value investors, this certainly looks like an attractive longer-term opportunity. Keep in mind, energy stocks are very volatile. They are price-takers rather than price-makers. If you don’t mind this and like a nice 5% dividend yield in the meantime, Suncor might just be the perfect contrarian stock to buy today.